Weekly Macro Summary 2/14/21

02/14/2021

THIS IS NOT INVESTMENT ADVICE.

Please speak with a registered investment advisor or other qualified financial professional before making any investment decisions.

Quote of the Week

“Good morning, Jamie. Just very quickly, I just want to say that the most interesting thing that's happening is the rate at which demand has increased. We've never seen an increase in demand happened as quickly. And that combined with COVID and the pandemic has really stretched the supply chain. Mark mentioned, we did have elevated freight costs in the fourth quarter of last year. And as he said, we expect those to continue through the first half. We are working with all of our suppliers. The supply base is generally tight, not just semiconductors, which has gotten a lot of press, but many of our components, are on longer lead times. Our suppliers and we are struggling with absenteeism due to COVID. And we are working very closely with our customers to remain connected and to continue to supply them as best we can. We are working through all of these issues on a daily basis, and the cost that we expect are included in our guidance. And we expect to be able to supply what we believe our market forecast is that Mark said earlier.”

-Tony Satterthwaite, President and Chief Operating Officer of Cummins Inc.

If you would like to receive the Weekly Macro Summary directly to your mailbox every Sunday, please subscribe. It’s free.

ECONOMIC DATA

“Healthy jump in indeed.com US job postings: +2.4% above pre-pandemic baseline as of Feb 5. Was +0.7% one week earlier, on Jan 29. Accelerating improvement! 1.7 %pt weekly gain is similar to last summer's recovery pace.”

-Jed Kolko, Chief Economist, indeed.com

In the United States, as of February 14, 38.3mln people had received at least one dose of the COVID-19 Vaccine.

Daily doses averaged 1.7mln per day. At the current pace, approximately 75% of the 16 & older population would be fully vaccinated by early September.

To date, approximately 36% of the 65 & older population have received at least one dose, an 8 percentage point increase week-over-week. At the current rate, more than 50% of the 65+ population will have received at least one dose by the end of Feb.

New daily confirmed cases of COVID-19 are down 22% versus a week ago and 60% from their peak while the positive test rate has halved in the past 6 months.

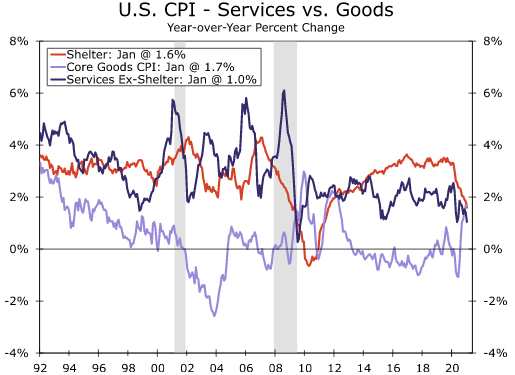

US consumer price index (CPI) for January +0.26%, y/y +1.37%.

Excluding food and energy, core CPI came +0.03% and +1.4% y/y.

Rent and owners' equivalent rent measures +0.11% m/m, in line with it's December increase.

Core goods prices +0.14% on the month.

Core services prices were flat on the month. Many of these are categories that remain weighed down by COVID developments (recreation services, airfares, and hotels) and we can expect an acceleration once broader vaccine distribution has been achieved.

Bottom Line: While market’s expect rising inflation rates over the course of this year, it’s still too soon to see signs of sustainably higher inflation.

China’s headline CPI for January -0.3% y/y versus unchanged expected.

Core CPI printed negative, -0.3%, for the first time since 2009.

Cause of the low print is weak travel activity and softness in healthcare and family services consumption.

US JOLTS Job Openings 6.64mln at the end of December, higher than consensus and up from 6.572mln for November.

Job openings were led by a pop in professional and business services (+296k).

The quits rate rose to to 2.3%, the highest level since the pandemic started.

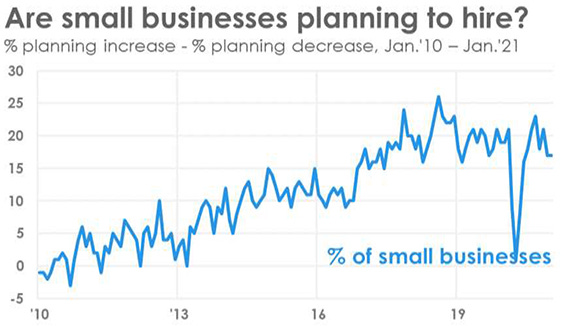

The NFIB Small Business Optimism Index at 95, down 1 point from December.

The 47-year average is 98.

“Owners expecting better business conditions over the next six months declined seven points to a net negative 23%, the lowest level since November 2013.”

“The net percent of owners expecting better business conditions has fallen 55 points over the past four months.”

Percent of owners thinking it’s a good time to expand, 8%.

Sales expectations over the next three months declined 14 points to a net negative 4%.

Despite some fall in sentiment and expectations, the employment measures remained strong

German industrial production was lower than expected +0.0% m/m (0.3%exp). Lockdown measures are weighing on industrial activity.

UK GDP +1.2% m/m for December, ahead of expectations of +1.0% and grew 1% q/q for Q4’20.

The UK economy is now around 7% below pre-COVID levels.

Manufacturing remained resilient while services saw a solid bounce back.

Household spending contracted in the quarter but was offset by government consumption and investment.

Mexico’s January CPI print above consensus +0.86% m/m (+0.77% m/m expected).

Annual rate is now +3.54% y/y but core inflation remains broadly unchanged.

CENTRAL BANKS

ECB President Lagarde spoke at the at the plenary session of the European Parliament.

“In this environment, an accommodative monetary policy stance remains essential.”

People’s Bank of China (PBOC) published their Q4’20 monetary policy implementation report.

Will prioritize policy stability with no sharp turns.

Will adhere to normal monetary policy, stable central bank balance sheet along with lower leverage and credit growth compared to the post-2009 period.

Fed Chair Powell: “We are a long way from a strong labor market.”

“Achieving and sustaining maximum employment will require more supportive monetary policy.”

Called for, “society wide commitment” to maximum employment.

Cleveland Fed President Loretta Mester said the Fed is, “going to be accommodative for a very long time.”

Dallas Fed President Kaplan:

Mass vaccination and additional fiscal stimulus will increase output, put downward pressure on unemployment, and temporarily lift inflation but the upward price pressures will not be persistent.

Sweden’s Riksbank kept policy unchanged and projects no changes in rates through 2024.

Reiterated that rate cuts are still possible if needed.

Expects the economy to return to normal levels in Q3’21, a quarter earlier than previously forecast.

Pace of bond purchases will slow to SEK100bn in Q2 (from SEK 120bln currently).

EQUITIES

Alibaba (Ticker: BABA), reported 3Q earnings in early February, the stock is up roughly 21% from a year ago and 18% ytd.

Sales rose 37% in 3Q, with cloud computing, retail and commerce leading. Cloud computing saw its first positive EBITA margin.

Alibaba reported 779 million active consumers in Q3.

Pfizer (Ticker: PFE), announced it will grow revenue 6% in 2021, excluding Covid-19 vaccine sales.

Sales were 3.3% lower than the consensus and EPS missed by 18%.

2021 Sales guidance of $59.4 - 61.4 billion was above expectations, but the midpoint EPS goal of $3.15 was below consensus due to much lower gross margin, decreased profit from the BioNTech profit share agreement and higher R&D costs.

Amazon (Ticker: AMZN), reported strong fourth quarter results on the back of increased online shopping and additional stimulus checks.

Q4 Sales rose 44%; online stores +46% and third-party seller services increasing 54% following strong holiday demand and moving Prime Day to the fourth quarter.

Amazon Web Services jumped 28% q/q.

Q1’21 revenue guidance of $100-106 billion, which is above consensus.

Management expects Covid-19 related costs to decline 50% to $2 billion q/q.

Google (Ticker: GOOGL), reported Q4 results in early February. The stock is up 21% ytd and 38% from a year ago.

Revenue surprised estimates by 5%, coming in at $46.4 billion, Adj. EPS for the quarter was 15.5 vs the consensus of 17.6. GAAP+ EPS was 19.24, a 23% positive surprise from the consensus.

Analysts believe YouTube Ads may benefit from a secular shift in brand advertising from traditional TV spending.

Cloud segment could see accelerated revenue growth in 2021 with increased enterprise usage.

Twitter (Ticker: TWTR), shares are up nearly 25% for the week after reporting strong Q4 earnings.

Analysts expect top-line growth to accelerate in 2021, mostly driven by increased advertisement spending as live events resume.

Revenue growth beat expectations by 8%, ending the quarter at $1.29 billion. GAAP EPS came in at 0.27 vs the consensus of 0.163, a 65% positive surprise.

Ad revenue gained 31% y/y driven by impression growth and price stabilization.

Monetizable daily active users grew by 1 million to 37 million in Q4.

Uber (Ticker: UBER) Q4 earnings highlighted a slow demand recovery for ridesharing and continued reliance on subsidies for an expanding delivery segment.

The company continues to cut costs and will divest from its unprofitable Freight business in an attempt to increase cost saving measures.

Revenue was $3.16 billion for the quarter which was 1.59% below expectations. Uber reported a net loss of $1.034 billion in the Q4, a 50% negative surprise from analysts.

Lyft (Ticker: Lyft) Q4 Revenue and Net Income beat consensus.

Q4 revenue of $569 million vs an estimated $561 million. Net Loss for the quarter was $180 million, beating estimates by 19%.

Ride volume continues its slow recovery, which may be down 40-50% in Q1. Lower driver incentives and continuous reduction in fixed costs could help the company achieve its goal of breakeven EBITDA in the second half of the year.

Walt Disney Company (Ticker: DIS) closed the week at a new all-time high $190.91. The company has experienced remarkable strength in their streaming platform.

Q1’21 EBITDA beat the consensus of $878 million by 148%, coming in at $2.2 billion.

The recent rise in the stock price can be attributed to Disney+, which shows no signs of slowing. The first quarter of fiscal year 2021 saw 21.2 million new users bringing the total number of subscribers to 94.9 million. The upcoming price increases may boost top line growth.

The Disney Parks operating income fell an additional $2.6 billion on limited capacity and extended closure in Paris and California. This news did not come as a surprise and with the vaccine rollout and pent up demand, analyst expect demand to pick up in the 2H.

Canopy Growth Corp (Ticker: CGC), reported strong Q3 earnings on Tuesday the 9th. Shares ended the week down 6.5% but not after being up 25% at one point. News organizations have dubbed this week's volatility a “reddit” fueled mania.

Net revenue has beat expectations for the third straight quarter, increasing 23% from the prior year, ending the quarter at $152 million

Recreational marijuana usage saw gross revenue increase 15% in Q3 from the prior year to $70 million and Medical marijuana usage saw an increase of 10% at the end of the third quarter from a year ago to $45 million

Non-GAAP Gross Profit was $40 million and EBITDA was -$68.4 million, a 3.8 percent positive surprise

GEOPOLITICS

The United States Senate has voted to acquit former President Donald Trump in his second impeachment trial on Saturday. With a vote of 57 yays and 43 nos, the final steps in the impeachment process have fallen short of the two-thirds required for conviction.

Former President Trump was charged with inciting the January 6th riot at the Capitol. Seven Republican Senators joined the Democrats in finding Trump guilty this time compared to just one in the first impeachment trial.

The second impeachment vote has the most Senate support since president Andrew Johnson’s 1869 impeachment trial.

The acquittal leaves the door open for Trump to make a 2024 presidential run. After already promising retribution in 2022 against Republicans who crossed him, polls show him damaged but still the front-runner among republicans.

Nobel prize winner and State Counselor Aung San Suu Kyi was arrested on Feb 1 by the Myanmar (aka: Burma) military (aka: Tatmadaw), citing alleged fraud surrounding the elections held in November of last year.

The coup came abruptly to most observers, seeing as Aung San Suu Kyi was somewhat of an ally to the military despite tensions, even personally defending the military mass killings of the predominantly Islamic Rohingya minorities during her International Court of Justice appearance in late 2019.

“The international community has repeatedly gotten Myanmar wrong … We got it wrong in the late 2000s when we thought the military had no intention to transfer authority to a civilian government; we got it wrong when it came to Aung San Suu Kyi and her authoritarian tendencies and attitudes toward ethnic minorities; and it seems we got it wrong when it came to this, too.” - Aaron Connelly, South-east Asia specialist, International Institute for Strategic Studies.

Approximately 384 of those in favor of the National League for Democracy Party have been arrested since and continue to be arrested in the face of mass amnesties of ex-convicts in Yangon. It is believed the move is to empty jail cells in preparation of further opponent crackdown.

In similar fashion to the 80’s and 90’s, protests have erupted, and civilians continue to resist despite being met with warning shots, water cannons, and largely unpredictable night time arrests.

The United States has issued sanctions, targeting a number of military generals, limiting US assets benefitting the Myanmar military as well as strong export controls and preventing access to the $1bln in Myanmar government funds being held in the US.

Mario Draghi has officially been sworn in as Italy’s next Prime Minister. Taking the oath on Saturday Feb 13, along with his 23 Cabinet ministers which consist of economic experts and various other career politicians spanning the political spectrum.

Draghi, 73, an MIT trained economist who led the European Central Bank from 2011 to 2019. Most famously known for leading the ECB through the euro-zone crisis in 2012.

The former Prime Minister, Giuseppe Conte lost control of the party after mis-handling the Covid-19 response.

Italy’s tourism accounts for roughly 13% of the country's gross domestic product, as the pandemic has taken a significant chuck from the economy. Draghi’s government will appoint a tourism Ministry from the previous culture ministry.

PUNDITRY

Marko Kolanovic, JP Morgan's head of quant and derivatives strategy,: "Commodity Supercycle and Related Equity Flows"

4 Commodity supercycles in the past 100 years. The last one started in 1996 and peaked in 2008.

The most important driver of that cycle was the rise of China and emerging markets.

During the period, USD weakened and commodities were more widely financialized. As a result, institutional investors embraced it as a new asset class that could diversify portfolio exposures.

JPM believes that 2020 marked the end of the commodity contraction and that we have now entered a new commodity super cycle. “Mostly it will be the story of a post- pandemic recovery (‘roaring 20s’), ultra-loose monetary and fiscal policies, weak USD, stronger inflation, and unintended consequences of environmental policies and their friction with physical constraints related to energy consumption and production.”

Inflation hedging characteristics: For the past decade, the global economy has experienced low growth and low inflation. The result was a bull market in bonds, bond proxies and secular growth stocks.

As inflation dynamics change and the theme of a resurgence in inflation becomes more widely accepted, JPM expects multi-asset portfolios to turn to commodities as a diversifying solution.

There are two drivers of the equity-bond correlation: volatility and inflation. All else equal, a regime of lower volatility and higher inflation weakens this correlation. This is what appears to be occurring as the world recovers from the COVID shock.

“In the period from 2010 to 2015, the Energy sector had a 10.6% allocation in equity portfolios. This has steadily declined to a 3.1% weight currently”.

During this period active managers reduced their allocation from 7% to 1.5%. The current US equity fund asset base is approximately $14trln. A re-allocation towards the energy sector would result in significant inflows and re-pricing.

Feedback

Thank you for subscribing to the Primary Dealer Review. If you have any questions or comments, please email me directly at primarydealer@weeklymacro.com and I will get back to you.

Do you know someone who would like to receive this publication? Please feel free to share the Weekly Macro Summary with them.

Legal Information and Disclosures

This weekly summary expresses the views of the author as of the date indicated and such views are subject to change without notice. The author has no duty or obligation to update the information contained herein. Further, the author makes no representation, and it should not be assumed that past investment performance is an indication of future results.

Moreover, wherever there is the potential for profit there is also the possibility of loss.

This weekly summary is being made available for educational purposes only and should not be used for any other purpose. The information contained herein does not constitute and should not be construed as an offering of advisory services or an offer to sell or solicitation to buy any securities or related financial instruments in any jurisdiction. Certain information contained herein concerning economic trends and performance is based on or derived from information provided by independent third-party sources.

The author believes that the sources from which such information has been obtained are reliable; however, it cannot guarantee the accuracy of such information and has not independently verified the accuracy or completeness of such information or the assumptions on which such information is based.

This weekly summary, including the information contained herein, may not be copied, reproduced, republished, or posted in whole or in part, in any form without the prior written consent of the author.