Weekly Macro Summary 01/17/2021

THIS IS NOT INVESTMENT ADVICE.

Please speak with a registered investment advisor or other qualified financial professional before making any investment decisions.

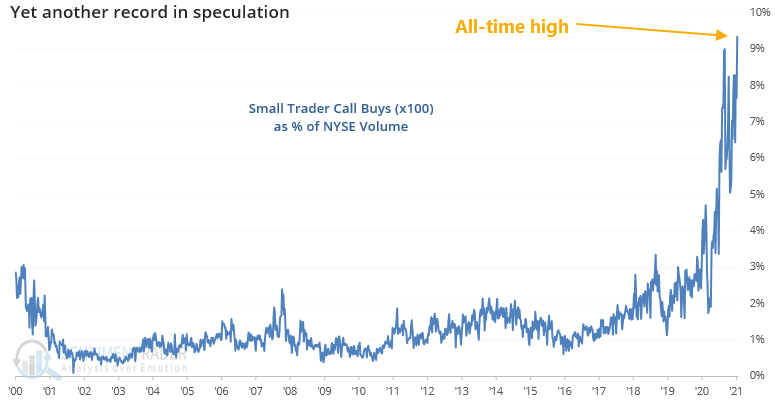

Chart of the Week

If you would like to receive the Weekly Macro Summary directly to your mailbox every Sunday, please subscribe. It’s free.

ECONOMIC DATA

Goldman Sachs, “The Re-opening at a Glance”

US headline retail sales for December weaker than expected, -0.7%m/m versus consensus at 0.

Core retail sales were even weaker, -2.3%m/m.

The bright side is that retail sales are still 2% above their February 2020 (pre-COVID) levels.

US CPI for December came in line with expectations, core CPI +0.09% m/m and 1.6% y/y.

Headline CPI +0.4%m/m and +1.4% y/y.

Why it matters: The Fed is committed to keeping the funds rate at 0 until they are able to average 2% inflation for some period of time. Still no price pressures although some base effects and disruptions are expected to create a transitory pickup in inflation later this year.

US JOLTS Job Openings little changed from November and in line with consensus at 6.53mln.

Quits rate unchanged at 2.2%, while the layoffs and discharges rate increased from 1.2% to 1.4%.

Number of Unemployed Persons per Job Opening

German first estimate of GDP -5.0% y/y for all of 2020 .

Suggests that the economy did not contracts in the 4th quarter despite a rise in restrictions.

Japan core machinery orders were very strong, +1.5%m/m versus -6.5%m/m expected, this follows a 17% rise in October.

Non-manufacturing orders (construction and telecommunications) were big contributors to the positive surprise.

Korea’s first 10-day average exports for January, +5.8%y/y.

Last week we highlighted the strength of December exports that confirmed strong economic trends in Asia.

China Export Growth +18%y/y in December versus +15% expected.

Stronger shipments to regional trading partners.

Imports +6.5%y/y vs +5% expected let by growth in high tech products and mechanical/electrical products.

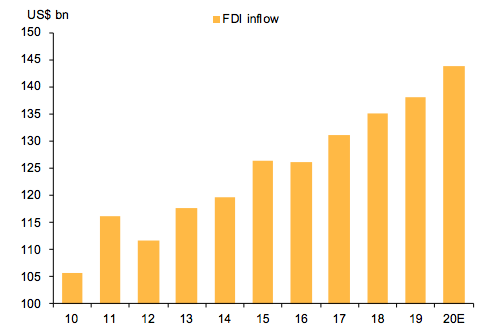

Annual Foreign Direct Investment inflows for China will reach a record high in 2020.

Foreign investors doubled their investment into China’s bond market to RMB 1.1trln in 2020.

China’s exports to the US grew by 8% in 2020 after a 12% decline in 2019 due to the trade war.

2020 is the second year that the EU replaced the US as China’s largest export destination.

“Amid all the noises on de-coupling and de-globalization, somewhat unexpectedly, the pandemic has deepened the ties between China and the rest of the world.” -Macquarie Bank

Source: Macquarie Bank

Source: Macquarie Bank

Australia’s November retail sales +7.1% m/m and up 13% from a year ago.

Why it matters: Victoria saw sales up 22%m/m as a result of economic re-opening. During the country’s shutdown, Australia had a savings rate of 20%. The remarkable boom upon re-opening could be a preview of what will happen in the US where consumers have also seen a significant amount of excess savings during COVID shutdowns.

Outook for Australia:

Similar to our general economic outlook, we expect Australia to see a boom in 2021 despite the dip into recession territory in Q2 following wildfires and coronavirus lockdowns. That said, there are some underlying data points that may hinder a strong recovery.

In a first in nearly three decades, Aussie GDP saw a contraction of -3.8% between Sep 2019-2020.

November saw rates cut to record low of 0.10% by the Reserve Bank of Australia.

While an extended recession was avoided for 2020, serious trade tensions with China increase risk going into 2021.

Despite this, BoA expects major fiscal support and household consumption following the reopening of the domestic economy will keep Australia positive in the coming year.

Following the UK, Australia has also implemented foreign investment rules, recently blocking a Chinese AUS $300M takeover of a domestic building contractor, CSCEC, in the name of “national security.” Such scrutiny of a smaller acquisition will likely send a message to Beijing that Canberra will be enforcing its new merger regulations.

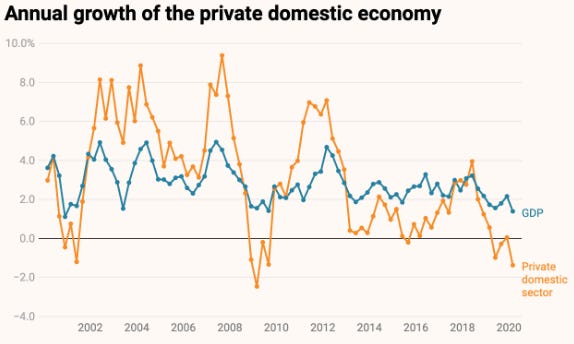

While annual GDP numbers have been overwhelmingly positive, government spending has allowed GDP to stay afloat despite less YoY growth in the private sector since 2013.

Source: Australian Bureau of Statistics

Household consumption growth in Australia has been well under the 25-year average, starting from 2013.

Source: Australian Bureau of Statistics

CENTRAL BANKS

Federal Reserve’s Beige Book, “Most Federal Reserve Districts reported that economic activity increased modestly since the previous Beige Book period.”

Strong shift from in person to online shopping this holiday season.

Auto sales weakened since the last report.

The energy sector expanded for the first time since the pandemic began.

Residential real estate remained strong.

“A growing number of Districts reported a drop in employment levels relative to the previous reporting period. Labor demand was strongest in the manufacturing, construction,and transportation sectors.”

Fed Governor Brainard: “outcome-based forward guidance communicates how the policy rate will react to the evolution of inflation and employment. It makes clear that the timing of liftoff will depend on realized progress toward maximum employment and 2 percent average inflation.”

Regarding asset purchases, “the December guidance clarifies that the pandemic asset purchases will continue at least at the current pace until substantial further progress is made on our employment and inflation goals. In assessing substantial further progress, I will be looking for sustained improvements in realized and expected inflation and will examine a range of indicators to assess shortfalls from maximum employment.”

"The economy is far away from our goals in terms of both employment and inflation,and even under an optimistic outlook, it will take time to achieve substantial further progress. Given my baseline outlook, I expect that the current pace of purchases will remain appropriate for quite some time."

Other US Federal reserve comments:

Fed Chair Powell: “now is not the time to talk about [ending asset purchases] ... when it does become appropriate for the committee to discuss we will let the world know.”

Kansas City Fed President George: “It is too soon to speculate about the timing of any change in policy.”

St Louis Fed President Bullard, regarding tapering bond purchase: “We are not close to that yet.”

Cleveland Fed President Mester: “A slowdown in the economy in the first part of the year along the lines I am expecting would not require a change in monetary policy so long as the medium-run outlook remains intact.”

Boston Fed President Rosengren: “for those whose incomes were not interrupted there is significant capacity to make expenditures once the pandemic is over ... we are likely to see a significant pick up in consumption.”

“It will be a while before we talk tapering.”

San Francisco Fed President Daly: “math of inflation would suggest that we’ll see some spikes in the middle of the year… [but] not at all worried that there’s this run-up in inflation around the corner that we will need to preemptively stave off.”

Market implied 1 month US treasury rate in 30 years time

Bank of England Governor Andrew Bailey shared his perspective of the potential for the BoE to implement negative rates.

He was skeptical of negative rates saying, “there are lots of issues with it”. Among those cited are the adverse impact on bank profitability which could curtail credit creation.

Sees the true unemployment rate at 6.5% in the UK versus 4.9% reported.

FIXED INCOME, CURRENCIES, COMMODITIES

Treasury rates were mostly unchanged on the week as a result of relatively strong 10 year and 30 year treasury bond auctions. 10 year yields are still up 18 basis points in the first 15 days of 2021. The lack of follow-through for higher rates this week was despite President-elect Biden’s release of a $1.9trln stimulus proposal for additional COVID relief. The proposal was called, “step 1”. In February, Biden will release “step 2” which will be focused on infrastructure spending.

The proposal promotes $1trln in income support via unemployment benefits and direct stimulus payments.

$1,400 stimulus checks cost ~$450bln. These are in addition to the $600 that was passed in December 2020.

Extension of enhanced unemployment benefits ($400/week) through Q3.

$15 per hour minimum wage.

$400bln for COVID-19 management.

$350bln of aid for state and local government.

$130bln for schools.

Crypto Outlook for 2021:

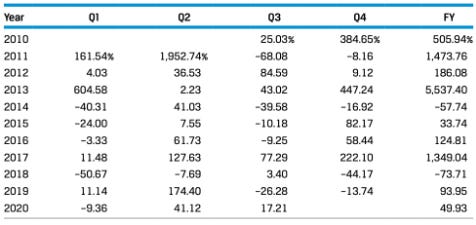

Cryptocurrencies have been a hot topic coming into the new year after a strong run in 2020. It’s clear that crypto and blockchain are not going away any time soon. At the time of this writing, the global crypto market cap stood at just over $1tln and Bitcoin, the world’s largest digital currency, had a market cap of $660bln. A $10,000 investment made in bitcoin in July 2010 would be worth over $5.8bln as of December 31, 2020

With high returns, comes high volatility. Bitcoin has experienced 15 negative-return quarters since its inception. The largest pullback was an 84% drop between December 2017 and December 2018. The table below illustrates bitcoin's quarterly and full-year returns ranging from 2010 to 2020.

Source: Bitwise Asset Management Until recently, bitcoin has had little correlation with other major assets. The following charts illustrate the low correlation between bitcoin and other risk asset classes since 2017. The light green band highlights correlation levels between -0.25 and 0.25. Dark green band highlights the range between -0.10 and 0.10 (considered negligible)

Source: Bitwise Asset Management

Crypto has achieved substantial institutional support over the past several months. Major financial institutions, large endowments, leading companies and central banks have expressed their support for the technology and in some instances have purchased cryptocurrencies for their investment portfolios.

In 2020 the largest coins by market cap did especially well: Bitcoin (BTC) was +305.07% and Ethereum (ETH) +563.72%. Moving into the new year, crypto assets will undoubtedly continue to stir conversation. With 2020 performance ending on a high-note for most crypto assets we wonder if this might be a year in which alt-coins receive a halo-effect from the institutional capital that has been deployed into the space.

EQUITIES

Small-cap stocks led the way higher for US equities this past week. The Russell 2000 was up 1.5% while the S&P500 fell 1.5%. The Russell 2000 is now approximately 40% above its 200 day moving average, a remarkable display of momentum. Concurrently, the short interest interest in the benchmark SPY ETF is now approaching the lowest levels of the last 10 years. This type of universal bullishness often serves as a contrarian signal.

Bank stocks got a drubbing on Friday led lower by Wells Fargo and Citi which were each down ~7%.

Wells Fargo earned 64 cents per share on $18bln in revenue. Both of those figures were in line with estimates.

Credit loss provisions down $823mln largely because of the sale of their student loan portfolio.

Citigroup’s reported earnings of $2.04 per share on revenue of $16.5bln. The earnings were a beat versus estimates but the revenue number was a disappointment.

JP Morgan earned $3.79 per share with $30.2bln of revenue versus estimates of $2.62 and $28.7bln.

Why did bank shares fall on Friday if earnings were ok? Since November 8th, Citi and Wells Fargo’s shares had both risen 44% on the expectations of significant improvement of their businesses as a result of a sustained economic recovery and enhanced profitability due to a steepening yield curve (a steeper yield curve typically boosts banks margins). With so much excitement surrounding the shares and the industry in recent months, market participants were anticipating significant beats of earning expectations.

Walmart is partnering with a financial-technology firm (Ribbit Capital) to create a new fintech start-up.

Details on the venture are scarce but the goal is to, “develop and offer modern, innovative, and affordable financial solutions to customers.

Ribbit’s current portfolio of fintech companies includes Robinhood, Credit Karma and Affirm.

Delta posted an earnings per share loss of $2.53 versus consensus expectation of a $2.50 loss.

Passenger revenue at $2.7bln in line with expectations (down 74% y/y).

Delta President Glen Hauenstein, “The early part of the year will be characterized by a choppy demand recovery and a booking curve that remains compressed.”

The company expects to be cash-flow positive in the spring and reiterated that forecast on their call.

GEOPOLITICS

Russia will be withdrawing from the international Open Skies Treaty.

The treaty permits aerial surveillance over military sites in 36 countries that are party to the treaty.

US formally withdrew in November citing repeated violations by Russia.

“This reflects a larger dismantling of the international arms control system that has helped stabilize relations between Russia and the United States since the Cold War, with New START -- the two countries’ last remaining major nuclear arms control treaty -- also set to expire next month” -Stratfor

Outlook: China, Taiwan, and Hong Kong

China can be expected to maintain prior growth and investment levels assuming world economic activities begin to normalize throughout the year. We believe that certain elements of 2020 will continue well into the next year for the region:

China has had no qualms with media censorship in 2020. The Alibaba probe coverage has since been restricted by Beijing officials as well as recent WHO officials that have made attempts to investigate coronavirus origins. The mysterious disappearance of Alibaba founder, Jack Ma, may serve as a precedent for Beijing to probe other major tech companies that speak out against the CCP.

Chinese crackdown on pro-democracy in Hong Kong will continue well into 2021 as city lawmakers loyal to the CCP remain unopposed.

In enforcement of Chinese national security laws imposed on HK last year, 53 pro-democracy politicians were arrested in the latest purge. With little opposition following a mass pro-democracy lawmaker resignation and waves of arrests, this latest iteration has been a clear escalation of what many have considered to be a threat to the freedoms promised in the change of hands from the UK to China in 1997.

In his final days in office, Donald Trump has imposed new sanctions on Beijing, condemning its treatment of HK. This follows a number of attacks against China including the blacklisting of several Chinese companies, preventing Americans from investing in those securities. Steven Mnuchin has pushed for China’s big three to be spared: Alibaba, Tenecent, and Baidu, in a revision to the original bill.

Taiwan made great strides to come out from under China’s watchful eye in 2020. We expect to see continued pushback from Taiwan while China tries to politically reign Hong Kong back in.

Recent pork trade has not gone well due to perception of US food regulations. Such perceptions have led local pork prices to skyrocket and thus price increases at restaurants and blowback on Tsai Ing-wen. That said, Taiwan has made significant gains towards removing hurdles for a bilateral trade deal should the country wish to continue in that direction.

Taiwanese companies operating in China have performed well in recent years. As China’s nationalist policies become more limiting and labor becomes more expensive, Taiwanese companies will likely move their operations from the mainland to create more jobs at home.

Source: Financial Times

Feedback

Thank you for subscribing to the Primary Dealer Review. If you have any questions or comments, please email me directly at primarydealerreview@gmail.com and I will get back to you.

Do you know someone who would like to receive this publication? Please feel free to share the Weekly Macro Summary with them.

Legal Information and Disclosures

This weekly summary expresses the views of the author as of the date indicated and such views are subject to change without notice. The author has no duty or obligation to update the information contained herein. Further, the author makes no representation, and it should not be assumed that past investment performance is an indication of future results.

Moreover, wherever there is the potential for profit there is also the possibility of loss.

This weekly summary is being made available for educational purposes only and should not be used for any other purpose. The information contained herein does not constitute and should not be construed as an offering of advisory services or an offer to sell or solicitation to buy any securities or related financial instruments in any jurisdiction. Certain information contained herein concerning economic trends and performance is based on or derived from information provided by independent third-party sources.

The author believes that the sources from which such information has been obtained are reliable; however, it cannot guarantee the accuracy of such information and has not independently verified the accuracy or completeness of such information or the assumptions on which such information is based.

This weekly summary, including the information contained herein, may not be copied, reproduced, republished, or posted in whole or in part, in any form without the prior written consent of the author.