Vaccine Approval in the West

12/13/2020

THIS IS NOT INVESTMENT ADVICE.

Please speak with a registered investment advisor or other qualified financial professional before making any investment decisions.

Commentary

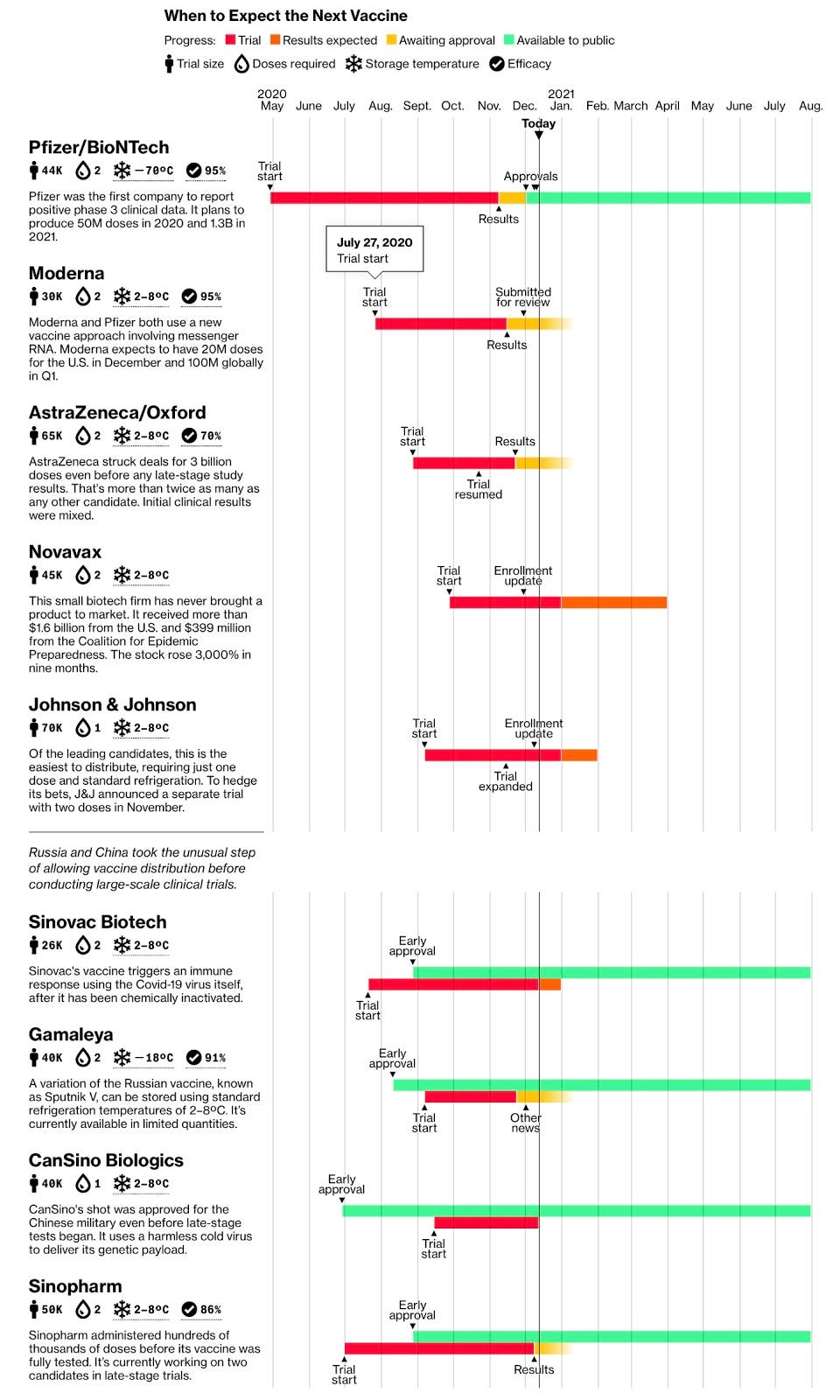

Pfizer and BioNTech’s mRNA-based vaccine has been approved for use in the United Kingdom, Canada, Bahrain, and Saudi Arabia, and has received emergency use authorization on December 11th from the FDA in the United States. In US trials, “less than two weeks after the first dose, the vaccine started protecting [recipients], and the second dose three weeks later boosted their immune response.” Vaccinations for front-line workers and high-risk groups are expected to start this coming Monday in the US and Canada, and have already begun in the UK.

As more research into the vaccines are being published, the percentage of US adults who would get a vaccine if it was available today is rising, with 60% saying that they would definitely or probably get the vaccine, up from 51% in September 2020, but down from 72% in May 2020. 75% of US adults have a fair amount or a great deal of confidence that the R&D process in the US will produce a safe and effective vaccine, however only 37% of respondents indicated that they would be comfortable being among one of the first groups to receive the vaccine, highlighting the safety and efficacy concerns that will need to be addressed by public health authorities.

Why it matters: We expect that the rapid vaccine progress, accommodative central bank policies, and rapid corporate/private sector adaptation to be the key drivers behind a strong rebound in overall economic growth and activity in 2021 and 2022.

What we’re watching: Progress towards herd immunity will be a key area to watch for the year ahead, as it will heavily influence the timing of business re-openings as well as government and central bank policy choices.

Chart of the Week

If you would like to receive the Weekly Macro Summary directly to your mailbox every Sunday, please subscribe. It’s free.

ECONOMIC DATA

Atlanta Fed GDPNow remained unchanged from last week at 11.2% for Q4.

New York Fed GDP Nowcast is currently at 2.45% for Q4 down from 2.52% last week.

US Consumer Price Index +0.2% m/m, +1.2% y/y vs 1.1% expected.

Staples like food and gas experienced declines m/m following a 0.2% increase in October, -0.1% and -0.4%, respectively.

Transportation services and apparel ticked up m/m, +1.8% and +0.9%, respectively.

Inflation does not appear to be a threat to investors or the economy as of now; the vaccine’s rollout and success might play a vital role in next year’s inflation tracking.

October JOLTS released Wednesday was little changed potentially signaling that the labor recovery from the pandemic was slowing.

+6.65mln job openings from +6.49mln in September, increasing job openings rate to 4.5% from 4.4%.

Hiring fell to 5.81mln from 5.89mln in September, lowering hiring to 4.1% from 4.2%.

Hiring experienced its biggest hits in wholesale trade and federal government.

The November Small Business Optimism Index shows small business owners remain uncertain after election.

NFIB Optimism Index -2.6% m/m to 101.4 vs 102.5 expected, remaining above the 47-year historical average of 98.

The University of Michigan’s Consumer Sentiment report highlighted a rise in US consumer sentiment and confidence in late November and early December.

Consumer sentiment +4.5 m/m to 81.4 vs 75.5 expected in the two weeks ended December 9, 2020.

Recent stock market performance and developing news on the coronavirus vaccines may help explain U of Michigan’s index gains.

US October consumer credit in October +$7bln vs $15.5bln expected

Smaller increase than $15bln in September. The shortfall is attributable to a $5.5bln decline in revolving credit. Non-revolving credit was +$12.7bln

China’s Consumer Price Index fell into negative territory in November for the first time since 2009.

November Headline CPI fell to -0.5% after a 0.5% rise in October.

CPI deflation mainly driven by improvements in food supply specifically pork and increased imports of the main source of protein for China.

“November’s CPI decline was driven by pork prices and should be short-lived…” said ANZ Economist Xing Zhaopeng.

CENTRAL BANKS

News of viable vaccines generating positive moves in the market is currently shifting economists’ views of recovery support including those of the European Central Bank (ECB), which has decided to launch a fresh stimulus policy on Thursday, laying very sensible groundwork for long-term support as we move into 2021.

€500bn increase (€1.35tn to €1.85tn) in its Pandemic Emergency Purchase Program (PEPP) as well as duration extension to the current policy by an additional nine months to March 2021

“Ms [Christine] Lagarde justified the nine-month extension to the stimulus programmes by the expectation that “we will have reached sufficient herd immunity to hope that by the end of 2021 the economy will function under more normal circumstances”. Analysts, however, interpreted the additional stimulus as a commitment to more long-term support and an admission that extraordinary policy could be needed for years. The ECB forecasts that inflation in 2023 will still be below its 2 per cent target.

The ECB has also extended its negative interest rate financing of banks (at rates as low as negative 1%) provided that they maintain the flow of credit. In effect, this policy pays the banks to borrow money and increase the availability of credit, as long as they don’t reduce lending. Internally at the ECB there are differing views between its governing council members - the initial proposal was to increase targeted longer-term refinancing operations (TLTRO) to 60% of the banks loan books (up from 50%), however the council eventually compromised at 55% (€300bln increase).

Perception of the decisions was “underwhelming” and a sign of “compromise between dovish and hawkish members of the governing council” per Frederik Ducrozet, a strategist at Pictet Wealth Management.

The ECB has cut its eurozone growth forecast for 2021 to 3.9%, based on the assumption that there would be no trade deal between the EU and the UK post-brexit.

The Financial Times this week posed the question “How long will the [US Federal Reserve] continue its extraordinary run of bond buying to keep interest rates down and support the economy in an effort to push inflation higher?”

As we’ve discussed in depth in the Weekly Macro Summary, Powell’s tolerance of inflation above the current 2% target has broader implications for the market, with much more downside risk associated with higher interest rates than there is remaining upside with accommodative policy.

“Already, market expectations of inflation are on the rise as the global economy pulls out of 2020’s shock on the back of enormous fiscal and monetary stimulus. In the US, long-term inflation expectations implied by the bond market have rebounded sharply from pandemic lows to their highest in 18 months.” (Financial Times)

The rising inflation expectations paired with depressed treasury yields has pushed down real yields well below zero, which, while good for risky assets like equities tends to usually put downward pressure on the dollar which we’ve seen recently.

Source: Financial Times, Refinitiv

FIXED INCOME, CURRENCIES, COMMODITIES

MicroStrategy, Inc., software company or Bitcoin fund? On Monday, the company announced its plan to offer $400 million of convertible bonds in order to buy more cryptocurrencies. On Friday, Michael Saylor, MicroStrategy’s CEO, tweeted that they raised $650m notional of a 0.750% Convertible Senior Notes Due 2025. The additional amount raised was due to strong demand for the offering.

This announcement comes only a few days after the company finalized the purchase of additional bitcoins. The company now has 40,824 on its balance sheet.

MassMutal Life Insurance Co. announced the purchase of $100 million or a 0.4% allocation in Bitcoins using their general investment fund. The 169-year-old life insurance company is the latest mainstream company to announce an allocation to cryptocurrency.

MassMutual also announced a $5 million dollar minority equity stake in NYDIG, a subsidiary of Stone Ridge, a firm that provides cryptocurrency services to institutions. NYDIC, which has roughly $2.3 billion in crypto AUM, will provide custody services for MassMutual’s Bitcoins.

On Thursday, the Bloomberg Commodity Spot Index rose 1.3% to its highest since 2014 on the back of vaccine approval news worldwide.

Demand for oil has strengthened due to the expectations that people will resume driving and traveling once a vaccine is widely distributed.

Soybeans and corn have increased sharply after dry crop weather in South America and Europe hit yields, all the while China is buying up massive quantities of farm goods from the U.S.

EQUITIES

Uber sells its driverless car business to Silicon Valley start-up company, Aurora.

The move is in response to Uber’s desire to finally become a profitable company.

In addition to the sale of the unit, Uber will get a 26% stake in Aurora for $400mln.

JD.com spun-off and took public its online health-care unit on Tuesday. Raised $3.5bln on a $34bln valuation.

Largest health-care IPO ever for Asia and shares rose 56% in their debut.

Shares offered to individual investors were 420x oversubscribed, those offered to institutional investors were 31x oversubscribed.

Monthly online consultations during COVID rose from 200,000 to 2mln.

JD’s valuation went from $7bln to $28bln during that time

Hyatt plans to add over 20 hotels to its existing European portfolio that currently consists of 63 properties. This is a vote of confidence from the company towards the prospects for the travel industry post-COVID. It also demonstrates a belief in the narrative that there is significant pent-up demand for leisure travel.

The planned expansion will focus on hotels geared toward leisure travel.

The first 20 hotels will cost approximately EUR900mln.

“We believe there is a pent-up demand to travel. Once we get the therapeutics, we get the vaccines and so forth there will be growth.”

The company currently operates 950 hotels worldwide.

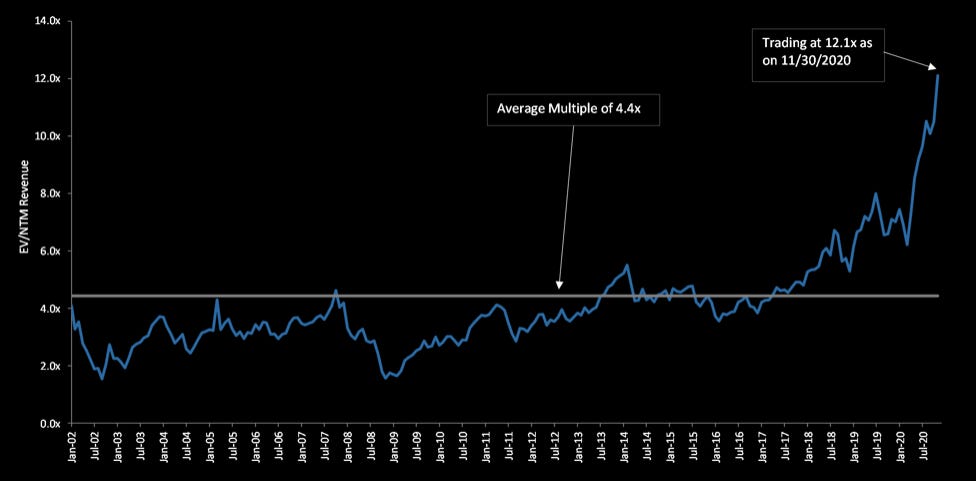

Software valuations at All Time Highs, currently trending 300% higher than average

The Federal Trade Commission of the US is suing Facebook for years of “anti-competitive conduct,” i.e. the acquisitions of Instagram (2012) and WhatsApp (2014). While different in specific allegations, this follows the recent antitrust litigation from the US federal court against Google (covered in our Vaccines, Volatility, Asymmetry, China, and Bitcoin issue).

Per FT: “Facebook’s actions to entrench and maintain its monopoly deny consumers the benefits of competition,” said Ian Conner, director of the FTC’s bureau of competition. “Our aim is to roll back Facebook’s anti-competitive conduct and restore competition so that innovation and free competition can thrive.”

Exchange-traded funds (ETFs) have added roughly $466bn, marking it the largest year of inflows to date. If the current trend continues, passively managed equities will surpass actively managed funds by the year 2022.

GEOPOLITICS

Britain began administering a covid-19 vaccine produced by Pfizer and BioNTech, two pharmaceutical companies. The first recipient was a 90-year-old woman in Coventry. A further 800,000 doses are to be dispensed in the coming weeks, with priority given to the over-80s and health and care staff. Meanwhile, Britain’s government announced that a different vaccine manufactured by Oxford University and AstraZeneca, another pharmaceutical company, was delayed due to manufacturing problems. Just four million doses will be available before January.

The UK intends on suspending tariffs against the US regarding their prior aircraft subsidies dispute (covered in our Two Americas issue) in order to prepare for trade talks with Washington in the face of a high probability of a “no deal” at the EU talks to be had today, Sunday Dec 13.

Given the UK’s departure from the EU, it was always unclear whether they would have maintained the EU’s aviation tariffs following Dec 31.

“With a no-deal outcome looming, the pound fell in choppy trading on Friday. Sterling slipped as much as 1.2 per cent in afternoon dealing, before trimming its losses to about 0.4 per cent to trade at $1.3241. It has shed 1.5 per cent over the past week in its biggest slide since September.”

EU planning new sanctions against Turkey during this period of increasing tensions in the Greece v. Turkey conflict in the Mediterranean. While initially the EU leaders intended to focus on the individuals linked to energy drilling off Cyprus, the list could be expanded.

“Turkey faces retaliation because it has carried out “unilateral and provocative activities in the Eastern Mediterranean” since EU heads of state and government warned Ankara in October about its behaviour, the summit document says. It invites EU member states to add to an existing sanctions list comprising two executives at a Turkish state-owned oil company “and, if need be, work on the extension” of the punitive measures.”

Indian farmers are up in arms over a new agriculture law, gathering in large protests in Delhi. Thousands of farmers have been protesting this week, pressuring the government to repeal the three recent agriculture laws and demand assurances of a minimum price for their crops.

Over 40% of India’s workforce is employed within the agriculture industry.

Feedback

Thank you for subscribing to the Primary Dealer Review. If you have any questions or comments, please email me directly at primarydealerreview@gmail.com and I will get back to you.

Do you know someone who would like to receive this publication? Please feel free to share the Weekly Macro Summary with them.

Legal Information and Disclosures

This weekly summary expresses the views of the author as of the date indicated and such views are subject to change without notice. The author has no duty or obligation to update the information contained herein. Further, the author makes no representation, and it should not be assumed that past investment performance is an indication of future results.

Moreover, wherever there is the potential for profit there is also the possibility of loss.

This weekly summary is being made available for educational purposes only and should not be used for any other purpose. The information contained herein does not constitute and should not be construed as an offering of advisory services or an offer to sell or solicitation to buy any securities or related financial instruments in any jurisdiction. Certain information contained herein concerning economic trends and performance is based on or derived from information provided by independent third-party sources.

The author believes that the sources from which such information has been obtained are reliable; however, it cannot guarantee the accuracy of such information and has not independently verified the accuracy or completeness of such information or the assumptions on which such information is based.

This weekly summary, including the information contained herein, may not be copied, reproduced, republished, or posted in whole or in part, in any form without the prior written consent of the author.