Powell Policy: Too much is better than not enough

Weekly Macro Summary 10/11/2020

THIS IS NOT INVESTMENT ADVICE.

Please speak with a registered investment advisor or other qualified financial professional before making any investment decisions.

Commentary

It has been widely reported that in 2008, during the heart of the financial crisis, the Treasury Secretary, Hank Paulson (a former Goldman Sachs CEO), was pleading with Speaker of the House Nancy Pelosi and Democrat leadership to support a proposed rescue package that Paulson and his team had constructed to save the American financial system. At one point, in a moment of levity, the former Goldman Sachs CEO kneeled in front of the Speaker for effect when asking for her vote. This past week the drumbeat of Federal Reserve policy makers pleading with Congress to pass a stimulus package continued to grow louder. Chairman Jay Powell put it this way, “Too little (fiscal) support would lead to a weak recovery, creating unnecessary hardship for households and businesses … By contrast, the risks of overdoing it seem, for now, to be smaller.” Powell, a former partner at private equity powerhouse, Carlyle Group, like Paulson, is begging for support for the economy. It’d be helpful if politicians were quicker to respond this time around.

Chart of the Week

Bank of America Weekly Economic Index - has activity flattened? Or worse, is it turning lower?

Bank of America

If you would like to receive the Weekly Macro Summary directly to your mailbox every Sunday, please subscribe. It’s free.

ECO DATA

Atlanta Fed GDPNow is currently tracking at 35.2% for Q3, up from 34.6% last week.

New York Fed GDP Nowcast stands at 14.0% for Q3, unchanged from 14.0% last week.

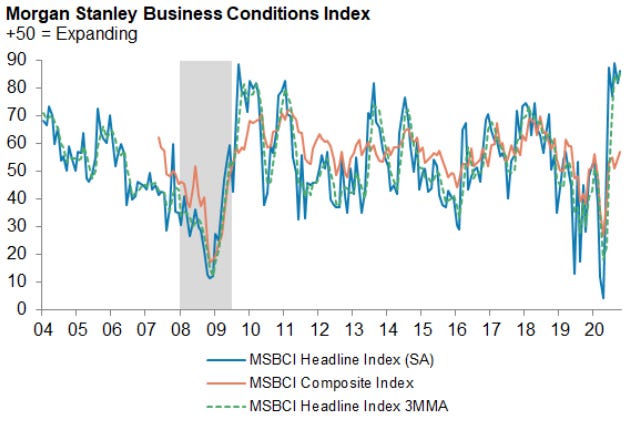

Source: Morgan Stanley

Source: JP Morgan

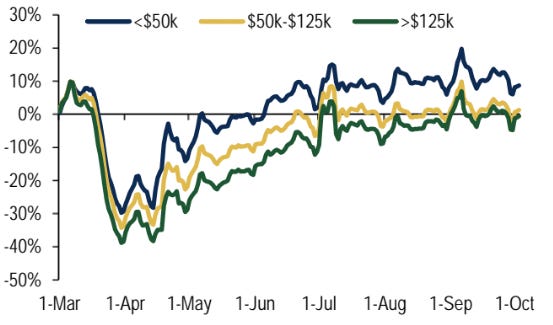

Daily total card spending by income group, (% yoy, 7-day moving average)

Source: Bank of America

US ISM Services index 57.8 slightly higher than 56.2 expected.

Employment subcomponent rises to 51.8 from 47.9 in August, back in expansion territory for first time since February. Means more firms reported hiring than cutting jobs.

Source: Citi

US commercial bankruptcy filings +33% ytd at 5,529.

September +78% y/y, 747 versus 420 last year.

Filings by individuals lower than last year thanks to government support.

United States Initial Jobless Claims +840K for the week ended October 3rd, a sign of slowdown in labor market recovery.

6th straight week at the 800k level.

More than 464K individuals applied for Pandemic Unemployment Assistance.

PUA covers workers that do not qualify for initial claims.

Job Openings in August: 6.493mln (Consensus: 6.5mn)

Down slightly from 6.697mln openings in July.

The quit rate fell from 2.4% to 2.2%

Firing rate fell 1.4% to 1.2%, pre-COVID average was 1.3%

Source: Quartz, USBLS

German manufacturing orders +4.5%m/m in August, stronger than expected (2.8% consensus).

The annual rate now -2.2% y/y in August, had been -6.9% y/y in July.

Source: Financial Times

Canada Housing Starts down 20.1% to 208,980 units from August’s 13-year high of 262,396 units.

Urban starts -21.1%.

Multiple urban starts -27%, single-detached urban starts +3.4%.

CENTRAL BANKS

On Tuesday Fed Chairman Powell reiterated the committee's plea for more fiscal support to boost the US recovery: “Too little (fiscal) support would lead to a weak recovery, creating unnecessary hardship for households and businesses … By contrast, the risks of overdoing it seem, for now, to be smaller. Even if policy actions ultimately prove to be greater than needed, they will not go to waste.”

FOMC minutes released on Wednesday.

Uncertainty about the outlook.

Emphasis on the importance of fiscal support.

A lack of fiscal stimulus is a significant downside risk to economic outlook, especially because the FOMC has factored in more fiscal stimulus into their projections for the economy in the coming year.

ECB minutes were released on Thursday with a notable, significant, item: the mention of EUR exchange rate.

"The recent appreciation of the euro exchange rate had had a material impact on the inflation outlook in the September ECB staff projections."

"It was considered important to avoid complacency and the perception among investors that the direction of exchange rate movements was a one-way bet."

"In the current environment of elevated uncertainty, significant economic slack and increased exchange rate volatility, the Governing Council would monitor incoming information very carefully and continue to stand ready to adjust all of its instruments, as appropriate, to ensure that inflation moved towards its aim in a sustained manner."

Euro Area Interest Rate

Source: TradingEconomics

Cleveland Fed President Mester: “I can imagine wanting to shift to longer-term Treasuries, as we did during the Great Recession, if we needed more accommodation […] at this point, given my forecast, I want this on the table but I haven’t built in a big increase from where we are now.”

Reserve Bank of Australia leaves rates unchanged but keeps a tone that implies the potential to expand bond purchases.

“The high rate of unemployment as an important national priority.”

“Continues to consider how additional monetary easing could support jobs as the economy opens up further”.

Bank of Japan maintains -0.1% short term rate and intends to keep the target 0% long term rate as determined by 8-1 vote.

Views on the economy are slightly upgraded by policymakers but remains in a “severe state” as business slowly begins to resume.

“The Japanese economy is starting to pick up and is likely to continue recovering partly due to continued fiscal and monetary stimulus” -Bank of Japan Governor, Haruhiko Kuroda

“Once the impact of the COVID-19 pandemic subsides globally, Japan's economy is likely to continue improving further as overseas economies resume steady growth”

Fabio Panetta, an ECB board member wrote a blog post entitled, “We must be prepared to issue a digital euro”.

Digital versions of currencies have been a hot topic for major central banks recently, hoping to address demand for electronic means of payment and fend off potential competition.

“A digital euro would complement cash, not replace it. Together, they would offer people greater choice and easier access to means of payment. This would help financial inclusion.”

A concern of this push for a digital currency is that this form of money might displace traditional deposits, emptying out commercial banks.

“...some people fear that a digital euro could hamper the activity of banks or generate instability in times of financial stress.”

FIXED INCOME, CURRENCIES, COMMODITIES

Legislation regarding the shift from LIBOR interest rate benchmarking to SOFR benchmarking for financial products have failed to pass, thus far.

While there are still 15 months to the proposed end of LIBOR, Wall Street originally expected legislative process to be completed this past Spring. The timeline has now possibly been moved to January 2021.

This shift has the potential to impact $200 trillion in securities and commercial transactions tied to the USD Libor.

Domestic Crude Inventories increased 501k barrels last week, climbing to the highest level since May.

“There continues to be uncertainty associated with domestic demand and the need for fiscal stimulus to continue to boost the economy and correspondingly boost demand for crude oil” - Rob Thummel, PM at Tortoise

Energy and exploration stocks rallied anywhere from 5% - 7% this past week.

Hurricane delta causes 540k b/d of offshore oil production in the Gulf of Mexico to shut down.

Strike actions by Norwegian energy workers and confrontations in Azerbaijan threaten to shut down 880k b/d of additional supply.

330k b/d threatened by Lederne oil workers association not being able to reach an agreement on employment terms (see below).

BTC pipeline carrying 550k b/d of Azeri oil has been targeted by Armenian forces.

Oil strike in Norway over wages and conditions threatens to reduce Norwegian oil and gas output by approximately 25% per Reuters.

“If the escalation of the strike goes ahead, crude oil and natural gas liquids will account for about 70% of the planned cuts with natural gas making up almost 30%, a Reuters calculation based on Norwegian output data showed.”

“A total of 966,000 barrels of oil equivalent per day is expected to go offline due to the strike by Oct. 14, triple the level so far, unless a deal can be reached to end the strike.”

“The strike has helped benchmark Brent crude rise LCOc1 above $43 a barrel this week and the prospect of more shutdowns was one of the factors behind a 3.1% jump on oil prices on Thursday, as well as higher gas prices.”

“The strike would also hit the fourth-quarter earnings of oil companies, with Equinor, Aker BP AKERBP.OL and Lundin Energy LUNE.ST likely to see reduced income per share of 4%-6% in the event of a 10-day strike, brokerage Sparebank 1 Markets said.”

“The union wants to match the pay and conditions of workers at onshore remote control rooms with offshore workers, as well as higher wage rises this year than proposed by oil companies.”

Loan listed funds have experienced significant outflows over the past 2 years, $85bln since 2018.

As a result fund assets have fallen to $77bln from $167bn.

This past week saw the biggest ETF inflow since January ($255mln).

Mutual funds now represent 6.4% of the S&P/LSTA Leveraged Loan Index, lowest level November 2010.

CLOs have bought almost ¾ of new loans issued over the last 12 months.

An interesting comment at this past week’s debate from Vice Presidential candidate, Kamala Harris, drove a significant rally in cannabis stocks this past week. She said, “We will decriminalize marijuana and we will expunge the records of those who have been convicted of nonviolent marijuana-related offenses.”

The once booming sector has been significantly out of favor this year. The MJ Index is down 38% from a year ago. Harris’s comments drove the index higher 11% this past week.

What’s most interesting to us is that the underlying company performance of some leaders in the industry are living up-to the previous hype just as investors have given-up

Canopy Growth Corp. (Ticker: CGC) has generated a Net Revenue of $399 million in FY 2020, up 76% over FY 2019. The stock has risen nearly 25% in the last six-months but is still down over 20% versus a year ago.

Aphria Inc., (Ticker: APHA) reported a Net increase in cannabis revenue of $55.6mln in Q3, an increase of 65% from the prior quarter. Aphria ended Q3 with $515.1mln of cash and cash equivalents, to fund planned Canadian and International growth. Until Harris’s comments, the stock was down 15% versus last year. The stock is up 65% in the last six-months and 30% this past week

Tilray, Inc., (Ticker: TLRY) saw quarterly Revenue Increase 126% to $52.1 million versus Q1’19 and 11% sequentially from the Q4’19. Tilray is now focused on achieving positive Adjusted EBITDA by the end of the Fourth Quarter of 2020. Tilray’s stock is down 75% versus a year ago despite a 25% rally this past week

As the industry sees positive growth and regulatory changes on the horizon, will the cannabis craze return?

Source: Bloomberg

Square Inc., has made a large investment in Bitcoin buying 4.7k coins, totaling $50mln or roughly 1% of their assets and will hold those coins on the balance sheet.

Square executed the purchase of the Bitcoins over a 24-hour period, using a Time-Weighted Average Price approach when low volatility and high market liquidity was to be expected. Square will custody the coins themselves. These details were outlined in a self-published whitepaper regarding the transaction.

CFO, Amrita Ahuja said the following: “We believe that Bitcoin has the potential to be a more ubiquitous currency in the future, For a company that is building products based on a more inclusive future, this investment is a step on that journey.”

Square is the 13th publicly traded company to hold bitcoin. The 13 companies currently hold $6.8bln in bitcoin or roughly 600,000 coins.

The Peoples Bank of China announced it will cut the reserve ratio for certain currency transactions made by financial institutions from 20% to zero.

The policy move provides capital relief to FX forward contracts and incentivizes banks to engage in currency transactions that align with the governments currency strategies

China also announced their willingness to facilitate reasonable growth of the money supply and social financing, while avoiding excess liquidity flooding in the market.

People’s Bank of China Governor Yi Gang, cautioned that excessive stimulus could lead to debt expansion and create asset bubbles that will increase longer-term systemic risks.

West coast wild fires have had a significant impact on Napa Valley furthering an already beleaguered tourist season because of COVID-19.

2018 tourist season saw 3.85mln visitors

The Liv-ex Fine Wine 50 Index, which tracks the daily price movement of the most heavily traded commodities in the wine market, has yielded investors 1.2% ytd, with a 5yr return of 26.14%. This market will be interesting to watch as the California wine industry faces unprecedented challenges.

EQUITIES

As of Tuesday, VIX (the benchmark volatility index) had closed above 20 for 158 trading days, the longest streak since during the global financial crisis. It’s unusual for volatility to stay elevated while the stock market rallies.

4th longest streak since the VIX’s inception.

We interpret the disconnect between elevated volatility and rising stock prices to mean that market participants still are not buying the, “economy is full healed and things are back to normal” theme.

Is elevated uncertainty and fear a good thing for stocks or a bad thing? Old Wall Street adage, “The Market climbs a wall of worry”

Morgan Stanley agreed to buy fund manager Eaton Vance for $7bln.

Expects to break even on an EPS basis immediately after the deal closes.

Will make Morgan Stanley the largest wealth and investment management platform in the world with a projected $26bln in revenue.

Expect cost savings of $150mln over time.

Morgan Stanley CEO, James Gorman, said on a conference call, “Our competitor Charles Schwab [SCHW] is trading at 20 times earnings and we’re trading at 10 times earnings. It makes absolutely no sense...Moody’s just upgraded us Friday night before this happened and this is clearly credit positive. If we traded at 14-15 times earnings, this stock would be a hundred bucks. We’re rerating Morgan Stanley.”

Bristol-Myers Squibb (BMY) to acquire MyoKardia, a heart disease specialist, for $13.1bln, a 60% premium the previous day’s closing price.

MyoKardia’s key product candidate is mavacamten, a drug that treats a thickening of the heart muscle that could be ready to market next year.

Google stated Monday that it will enforce rules that require app developers distributing Android software on the Google Play Store to use its in-app payment system.

Developers have until September 30, 2021 to use Google’s billing system, which takes a 30% fee from payments, instead of independent payment systems.

This will bring Google Play’s policies in line with Apple’s App Store policies.

This will better position Google to compete with the App Store’s revenues

Total App Store spending was $32.8bln in the first half of 2020 vs. Google Play’s $17.3bln

App Store spending increased 24.7% YoY, while Google Play grew only 21% YoY

Levi Strauss & Co. reported stronger than expected Q3 financial results

Adjusted EPS $0.08 vs. -$0.22exp. and revenue at $1.06bln vs $822.2mln expected

E-commerce revenue +52%!

Total available liquidity of $2bln with cash at quarter end at $1.4bln

Levi is remaining cautious, holding the expectation that its business will continue to be adversely impacted for at least the remainder of the year. The company came public last August and the stock has fallen 31% since the close of its first day of trading

IBM announced plans split. It will spin off some of its lower-margin lines of business to focus on the cloud business

IBM's revenue has generally declined since 2011, struggling to adjust to a quickly changing market.

Legacy business segments such as Global Technology Services has seen revenues fall from $9.01bln in 2Q 2014 to $6.32bln in 2Q 2020

Cloud & Cognitive Software have provided strong growth with Cloud & Data Platform up 29% in 2Q 2020, led by the recent acquisition of Red Hat

The split is expected to be completed by the end of 2021.

GEOPOLITICS

Russian Ambassador to Tehran Levan Dzhagaryan said that his country recognized the expiration of UN arms sanctions against Iran on October 18 and is ready to supply the county with its S-400 air defense system

The addition of the S-400 system to the Iranian arsenal would greatly enhance its military capabilities and could pose a threat to US-built aircraft flown by the US and its regional allies in case of conflict with Iran.

Zambia is widely expected to default on external debt commitments when it misses a $118mln interest payment coming due.

The country requested a freeze on payments on September 30 but bond holders rejected the request. Government revenue is reportedly down 1/3 as of the 2Q'20.

The country received a write off of its debt in 2005 but the IMF has refused to provide relief thus far. They have stated that the Zambian government has not taken any steps to realign economic policies and reduce public spending despite being encouraged to do so over the last several years

The mining sector accounts for 70% of Zambian exports

Public sector debt-to-GDP ratio stood at 91.6% at the end of 2019

Their external debt service requirements will be $1.6bln of interest payments in 2020 and 2021 (slightly over 7% of GDP) and $2.34bln in 2022.

China is the country's largest creditor and political leaders across the world will be monitoring the situation closely. China has been a significant creditor to many frontier economies.

The extent of China's claims on Zambia is unknown but some estimates peg the total at 1/3 of the Zambia's external debt

Most of the loans from China are provided towards the construction of domestic infrastructure. Countries will be watching to see what sorts of recourse China demands.

Policy hawks were skeptical at the time that many of the loans were made as the terms were onerous and appeared to be designed to fail in order to provide China leverage over the country’s policy and political direction

PUNDITRY

Stephen Roach, former Chairman for Morgan Stanley Asia

"A crash in the dollar is likely and it could fall as much as 35% by the end of 2021."

The cause of the significant fall will be due to a combination of collapsing domestic saving and a growing current account deficit.

"2Q domestic saving plunged back into negative territory for the first time since the global financial crisis”

“Going into the pandemic, the net domestic saving rate averaged just 2.9% of gross national income from 2011-19, less than half the 7% average from 1960 to 2005.”

“As budget deficits pile up in the years ahead, downward pressure on domestic saving will intensify.”

“The US is, in effect, liquidating the net saving required for the expansion of productive capacity. Without borrowing surplus saving from abroad, growth becomes impossible. The current account deficit will only deepen.”

As a result of all of this, Roach expected lenders to the US to demand concessions to finance this significant amount of debt. This usually happens with either an interest rate and/or a currency adjustment.

“The US Dollar index fell 3% in real terms both in the 1970s and the mid-1980s, and another 28% from 2002-11. During those three periods, the net domestic saving rate averaged 4.9% (versus -1.2% today) and the current account deficit was -2.5% of gross domestic product (versus -3.5% today).”

Andrew Tilton, Chief Economist for Asia at Goldman Sachs

"We think Asia's really the best positioned of the major regions right now, just given the good control of the virus in most of the regions outside of India and some parts of Southeast Asia”

"We just had a round of purchasing managers indices which were almost all better month-on-month, suggesting that industrial sector momentum remains pretty good"

"In China, stimulus was less focused on providing income replacement to the consumer than for example what we saw in the US...You do see relatively more sluggish recovery in consumer spending there, but I think given the good control of domestic transmission of the virus in China, we are seeing services activity come back there as well. It is farther behind than manufacturing, but it is recovering”

"In the event we have a Blue Wave...we think the prospects for a very large fiscal stimulus are probably bigger and that would have positive effects on growth but that would ultimately pull forward the ultimate timing of a Fed rate hike”

"We are still reasonably upbeat on the economic recovery going into 2021."

Bank of America

The space economy will likely grow to become a $1trln industry in the next decade driven primarily by new spending by the United States Space Force.

"In our view, the space economy will likely grow by over $1tn in the next decade alone. While the COVID-19 pandemic has led to delays in some public and private programs (Arianespace, Rocket Labs, ESA), the outbreak has not appeared detrimental to overall investment"

"In the United States alone, defense spending has been steadily rising for the past 15 years, and the beneficiaries are mostly publicly traded and private companies"

Legal Information and Disclosures

This weekly summary expresses the views of the author as of the date indicated and such views are subject to change without notice. The author has no duty or obligation to update the information contained herein. Further, the author makes no representation, and it should not be assumed that past investment performance is an indication of future results.

Moreover, wherever there is the potential for profit there is also the possibility of loss.

This weekly summary is being made available for educational purposes only and should not be used for any other purpose. The information contained herein does not constitute and should not be construed as an offering of advisory services or an offer to sell or solicitation to buy any securities or related financial instruments in any jurisdiction. Certain information contained herein concerning economic trends and performance is based on or derived from information provided by independent third-party sources.

The author believes that the sources from which such information has been obtained are reliable; however, it cannot guarantee the accuracy of such information and has not independently verified the accuracy or completeness of such information or the assumptions on which such information is based.

This weekly summary, including the information contained herein, may not be copied, reproduced, republished, or posted in whole or in part, in any form without the prior written consent of the author.