Diverging Fortunes - The Rising Tide Doesn’t Lift All Ships

9/27/2020

THIS IS NOT INVESTMENT ADVICE.

Please speak with a registered investment advisor or other qualified financial professional before making any investment decisions.

Commentary

The theme of this week’s report is the stark contrast in the economic recovery for individuals, industries, and countries. We explore the dramatic difference in performance for sectors of the labor market as well as the stock market in what the media has labeled a, “K shaped” recovery because some have made a complete recovery while others are still at or near their low points.

Chart of the Week

Source: Ernie Tedeschi, Evercore ISI

If you would like to receive the Weekly Macro Summary directly to your mailbox every Sunday, please subscribe. It’s free.

EQUITIES

The S&P500 is up 3.6% year to date while the Nasdaq-100 is up 28.4%.

Energy stocks and financials are the laggards, down 47% and 22% respectively.

A bright spot in the field of energy has been solar stocks which are up 87% ytd.

Technology and consumer discretionary are the best performing sectors up 26% and 16% respectively.

A theme that we’ve consistently covered here in the weekly summary - the US housing market - has seen its underlying economic strength translate into significant equity gains.

Stocks tied to US construction and housing are up 22% so far this year and just shy of 100% since the end of 2016.

Railroads are doing well this year. The average of the large rails that we follow are up 15.6%.

Rails are a cyclical industry whose performance tracks the amount of economic activity in the country. We view the year to date returns as an important leading indicator and market-based sentiment measure. It points to the expectation of a continued recovery of economic activity. At their nadir in March, these stocks were down almost 40% for the year!

To track the market’s views on recovery from COVID-19 and the permanent impact it may have on the economy we are keeping a close eye on airlines and hotels.

Stocks tied to the airline industry are down 47% year to date. While railroads demonstrate a belief in a sustained economic recovery, the lagging airline industry demonstrates the market’s belief that coronavirus’s impact on consumer willingness to travel will not be recovering any time soon and that the damage caused may be a permanent impairment to the industry’s current capital structure.

Stocks tied to the lodging and hotel industry that we track are down 27% ytd.

We don’t think that peoples’ fundamental desire to travel and go on vacation has been permanently impaired.

We expect the trends in hotels, airlines, and other stocks that are languishing because of COVID protocols to recover once people feel safe. Expect these stocks to respond closely to positive developments in treatment and vaccine efforts.

Growth stocks continue to outpace value stocks, +18% versus -13% year to date, continuing a multi-year trend in which investors continue to pay a premium for growth stocks in a world that has seen muted economic growth. Since the end of 2015 that difference is +110% for growth versus +40% for value.

Source: Capital Economics

Source: Strategas Research

Most active fund managers in the US failed to beat the market over the past year.

Overall, 67% of the actively managed domestic US equity mutual funds were beaten by their benchmarks

Over the past decade, “both growth and value funds underperformed their benchmarks” -S&P Global

Exception for Mid-cap and small-cap focused funds where at 56% and 53% respectively outperforming their benchmarks.

Steady rise of passive strategies continues to reinforce a weak period for active managers that has continued for over a decade.

Cruise Lines, (Royal Caribbean, Carnival, Norwegian) Shares of cruise operators responded positively to a research piece by Barclays upgraded that upgraded the sector to overweight from equal weight.

Barclays is calling the worst over for the sector and next week’s CDC decision on the no-sail order will be a catalyst for the stocks.

Norwegian +7.8%, Carnival +6.3%, and Royal Caribbean +5.3%.

The cruise industry has reported strong bookings for the second half of 2021 which confirms our belief that the travel industry has not been fundamentally impaired on a permanent basis. It’s a race between a recovery from the virus environment and the companies’ ability to stay solvent.

BP, Covid-19 concerns outweigh optimism regarding energy transition plan.

Since CEO Barnard Looney’s presentation to shareholders regarding the UK oil and gas pivot toward renewables, shares have continuously fallen

Closed at 232.4p on Thursday, the lowest level since October 1995, -53% ytd

BP announced in August it planned to cut oil and gas production by 40% and increase low-carbon investment 10x by 2030. It also promised to generate returns of 8% - 10%, less than traditional hydrocarbon investments but substantial compared with other clean-energy projects.

The plan was more conceptual and lacked actual detail about how BP plans on meeting such targets.

As a result of the pandemic, BP has been aggressive in trying to bolster its balance sheet.

Cut dividend in half

Reduced capital expenditures by $3bln

Issued a $12bln debt issue in June

10,000 job cuts.

ECO DATA

Atlanta Fed GDPNow is currently tracking at 32.0% for Q3, unchanged from 32.0% last week.

New York Fed GDP Nowcast stands at 14.1% for Q3, down slightly from 14.3%% last week.

Source: JP Morgan

Existing home sales for August, 6mln annualized rate, matches consensus expectations and strongest pace since 2006.

Sales rose in every region of the US and now back to pre-COVID levels across the country.

Median home price +11.4% y/y is the strongest since 2013. The bottleneck in the housing market is a lack of inventory.

Inventory of homes available for sale is down almost 19% from last August.

August new home sales hit a 14-year high, 1.01mln units (annual rate) sold vs 890k expected. Up 43% versus last year.

Prior month revised higher from 965k from 901k.

Months supply declined to 3.3 from 3.6.

MBA mortgage applications +7% last week and up 86% y/y, refinance accounts for 64% of the loans.

On Tuesday, KB Home (KBH) reported its strongest Q3 order book growth since 2005 (+25% y/y)

Backlog of homes contracted to be built but not completed +8% and now at the highest levels since 2007

Why is the housing market unstoppably hot? 30-Year mortgage rates near all time lows (2.90%), labor market for those with incomes over $60k almost back to pre-pandemic levels, and secular trend of household formation for millennials.

Source: Citi

Source: WSJ

Richmond Fed Manufacturing stronger than expected, +3 points in August to 21, (consensus expected a 6 point decline.)

Vendor orders and employment are at a 2 year high.

Source: Richmond Federal Reserve Bank

US preliminary manufacturing PMI: 53.5 from 53.1 while services PMI: 54.6. Both in line with estimates.

Employment subcomponents at 54.4 in services and 52.6 in manufacturing.

Indication of rehiring across industries and in line with broader employment figures.

For employment, PMIs indicated a contraction in hiring during May and June (number below 50) despite improving private payrolls reports.

Noteworthy strength in US services when contrasted versus Europe (see below).

The Eurozone preliminary manufacturing PMI 53.7 in September versus 51.7 in August.

Eurozone Services PMI back into contraction at 47.6 from 50.8.

German manufacturing 56.6 (52.2 est, highest since June 2018), services PMI 49.1 (53.0 est).

France manufacturing 50.8, Services PMI 47.5 (51.9 est).

UK manufacturing 54.3 (in line), Services PMI 55.1.

Japan manufacturing 47.3, Services PMI 45.6.

Bottom Line: Overall a mixed bag for the global PMI data with disappointment out of services PMIs that conflicted with optimistic business surveys. Hard to draw a concrete conclusion.

Source: JP Morgan

US initial jobless claims to 870k from 866k a week ago.

Continuing Jobless Claims down to 12.58mln from 12.78mln last week.

US Durable goods orders +0.4% m/m for August weaker than +1.5% expected.

Core capital goods orders +1.8% above 1% expected.

Orders for durable goods excluding transportation now back to pre-COVID levels, orders for nondefense capital goods (excluding aircraft) now above pre-COVID levels.

Global car sales are experiencing a sharp recovery in Q3. By the end of August they had rebounded 68% from the low point of the year.

Fell 44% between December and March.

US Sales up 75% from the low point in April.

Source: Macquarie Bank

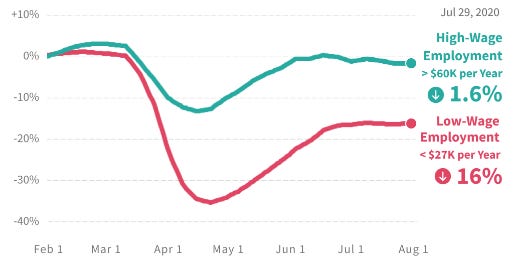

What is fueling the so-called, “K-shaped” recovery? The state of the labor market is vastly different for middle to high income earners versus those in lower income brackets. As new home sales soar to a 14-year high, auto sales rebound sharply and retail sales exceed their pre-COVID levels, we think it will be critical to watch the employment numbers and distribution of the recovery for various wage earners.

We noted in our August 23rd summary that High-Wage Employment (>$60K per year) fell just 0.5% by the end of June from pre-pandemic levels. That number has weakened slightly to 1.6%, while Low-Wage Employment has not improved at all. Can the economy continue to recover if this bifurcation in the labor market persists?

Source: Ernie Tedeschi, Evercore ISI

Source: Opportunity Insights

CENTRAL BANKS

Swiss National Bank leaves rates unchanged, threatens more intervention to cap appreciation of the Swiss Franc.

"In view of the fact that the Swiss franc is still highly valued, the SNB remains willing to intervene more strongly in the foreign exchange market, while taking the overall exchange rate situation into consideration... The low interest rates provide favorable financing conditions and, coupled with the SNB’s willingness to intervene, counter upward pressure on the Swiss franc."

Norway's central bank left rates unchanged and provided forward guidance that their base rate would be at today's level for “some time.”

Hungarian central bank raises rates from 0.6% to 0.75% in order to combat weakness in their currency, the Forint.

Turkey surprised markets with a rate hike. Move their benchmark rate from 8.25% to 10.25% to stem outflows and try to short circuit the currency’s depreciation (see Geopolitics section for more).

First hike since 2018.

The Turkish Lira is down 29% ytd and despite the surprise rate hike, the currency sold off 1% this past week. We continue to think that the story could be a canary in the coal mine for emerging markets. The Mexican Peso and the South African Rand each fell ~5% this week.

Local currency emerging market bonds fell 3% and dollar denominated EM bonds fell almost 2% this past week.

Ticker symbol: EMLC can be used to roughly track local currency emerging market bonds.

Ticker symbol: EMB can be used to roughly track US Dollar denominated EM bonds.

Source: BofA

FIXED INCOME, CURRENCIES, COMMODITIES

September 2-year Treasury auction, $52bln, is slightly weaker than August

Auction price was awarded close to fair value, 0.134%

Bid-to-cover 2.42 vs 2.78 in August, and previous 10 auction average of 2.58

Indirect participation down 5 points to 52.5%,

September 5-Year Treasury auction, strong demand

Auction was awarded 1 basis point below fair value (people, “paid-up” to get the issue), 0.275%

Bid-to-cover slightly weaker than last month at 2.52 vs 2.71 previously but still stronger than recent auctions.

September 7-year Treasury auction ($50bln) awarded at 0.462%, almost exactly the pre-auction fair value.

Bid-to-cover slightly weak at 2.42 versus the previous 10 auctions average of 2.51.

Otherwise solid result

U.S. crude oil imports averaged 5.2mln b/d last week, up 160,000 b/d from the previous week.

")

Propane has been the US’s largest petroleum export, 1.2mln b/d through June 30.

+17% y/y versus the same period 2019

Catalyst was Chinese-issued waivers for tariffs on U.S. liquefied petroleum gases.

Japan, South Korea, and China took delivery of 56% of propane exports.

US. total petroleum products exports

million barrels per day

6.0

50

4.0

3.0

2.0

Jan-Jun 2020 vs 2019

million barrels per day

gasoline

residual fuel

Oil

distillate fuel

oil

kero-tyR jet

all other

products

other HGL

2000 2004 2008 2012 2016 2020

Note: HGL = hydrocarbon gas liquids

Source: US. Energy Information Administratim, Petroleum Supp& %nthly

0.15")

US Motor gasoline exports still weak. Averaged 735k b/d, down 17% y/y versus 2019.

Domestically, regular gasoline prices decreased 2 cents from the previous week to $2.17 per gallon (national average) on September 21.

GEOPOLITICS

Chinese president Xi Jinping announced at the United Nations that his country will aim to cut its net carbon footprint to zero by 2060.

China is single-handedly responsible for 1/4 of the world’s greenhouse gas emissions.

If China succeeds, the global temperature in 2100 could be up to 11% lower compared to the current trajectory (Analysis from Carbon Action Tracker_

Reaching this goal will require a major shift in the country’s energy system, including elimination of their coal-fired power plant facilities, many of which are new construction.

China’s post-Covid stimulus spending on fossil fuels is three times larger than its spending on clean energy. Nearly $25bln spent on coal power plants.

Profitability of the coal business in China has been undermined by the potential early retirements of the current plants, plus the hundreds planned for the years before 2030, that may be forced to close ahead of schedule.

Source: Quartz

Uganda, Tanzania, and Rwanda are merging their stock markets electronically to ease the cost and time difficulties of cross-border trading. The project has been in development for almost 10 years.

When completed, local investors will be able to buy and sell stocks across those three countries without the currently existing hurdles, i.e. needing different stockbrokers in each country.

Project is funded by the World Bank.

Expected to become operational by the end of the year.

Will create a stock exchange with a combined market cap of around $15 billion.

Total of 54 listed companies, including Kenyan financial services companies, KCB Group and Equity Group as well as Nairobi-headquartered East African Breweries. They will be among the most valuable listed companies despite Kenya’s non-participation with the merger.

International healthcare companies are struggling to reclaim ~$2.3bln in debts owed to them by Turkey’s state hospitals, a senior US official has revealed.

“Companies will consider departing the Turkish market or will reduce their exposure to the Turkish market. This is not a direction that serves the interests of Turkey, its business persons or its citizens and it needs to be addressed and addressed promptly,” David Satterfield, US ambassador to Turkey.

New entrants to the Turkish market have been increasingly deterred in recent years by concerns about economic policy under the leadership of president Recep Tayyip Erdogan.

His leadership has been marked by an erosion of the rule of law and geopolitical risks caused by tense with Europe and the US.

Volkswagen had been close to finalizing an agreement to build a new car plant in Turkey last year but put the plan on hold after Mr. Erdogan ordered a military operation against US-backed Kurdish forces in north-eastern Syria that provoked outrage in Europe. The plan has since been canceled completely, citing the coronavirus crisis.

PUNDITRY

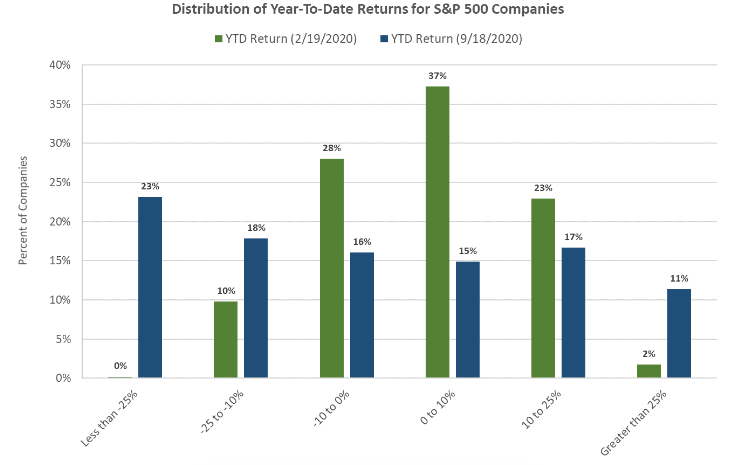

In past weeks (and the section above) we have summarized how the market has been behaving rationally in allocating money to winners and losers during the COVID downturn. In a piece entitled, “The Stock Market Is Less Disconnected From the ‘Real Economy’ Than You Think”, Nathan Tankus does a stellar job of diving further into this idea by contrasting year to date equity returns against year to date company performance:

Source: “Notes on the Crises”, Nathan Tankus

Citi: A contentious outcome of the US election is an underappreciated risk.

Orderly elections and a peaceful transition of government are a hallmark of American democracy.

Only 3 elections in US history had contention after election day: 1800, 1876 and 2000.

A combination of circumstances suggests that there is heightened risk of another contentious US election outcome.

Political and social polarization.

Concerns about voter suppression and voter fraud.

Logistical challenges and the potential involvement of courts and political bodies in deciding the election outcome.

Implications of a contentious election outcome range from prolonged uncertainty about the election outcome, to constitutional tensions to potentially even broader social unrest and protests.

Current composite Electoral College projections suggest a close race.

No Republican has won the presidency without Florida since Calvin Coolidge in 1924.

Biden’s national average polling lead is similar to Clinton’s heading into Election Day in 2016.

Margin of error remains significant, especially on state level polling.

Turnout amongst key demographics will likely determine the election.

Election Timeline:

November 3, 2020: US Presidential and Congressional elections are held.

Mail-in ballots must arrive and be postmarked by this date for most states (including toss-up states).

December 8, 2020: Deadlines for states to resolve election disputes (e.g., recounts, court contests).

“Soft” deadline but in 2000 Bush v. Gore became a key issue that pushed case to the Supreme Court.

December 14, 2020: Meeting of the Electors to cast ballots for President and Vice President.

December 23, 2020: “Hard” deadline for receipt of ballots.

January 3, 2021: First day of the new Congress (117th United States Congress).

January 6, 2021: Congress meets to count the electoral votes.

January 20, 2021: Current Presidential and Vice Presidential terms end.

Legal Information and Disclosures

This weekly summary expresses the views of the author as of the date indicated and such views are subject to change without notice. The author has no duty or obligation to update the information contained herein. Further, the author makes no representation, and it should not be assumed, that past investment performance is an indication of future results.

Moreover, wherever there is the potential for profit there is also the possibility of loss.

This weekly summary is being made available for educational purposes only and should not be used for any other purpose. The information contained herein does not constitute and should not be construed as an offering of advisory services or an offer to sell or solicitation to buy any securities or related financial instruments in any jurisdiction. Certain information contained herein concerning economic trends and performance is based on or derived from information provided by independent third-party sources.

The author believes that the sources from which such information has been obtained are reliable; however, it cannot guarantee the accuracy of such information and has not independently verified the accuracy or completeness of such information or the assumptions on which such information is based.

This weekly summary, including the information contained herein, may not be copied, reproduced, republished, or posted in whole or in part, in any form without the prior written consent of the author.